Examples¶

This page highlights some possible use cases of Pychastic package.

Simple Brownian motion¶

Brownain motion of a particle in one dimension is where SDE’s started. In this example there is no drift and noise is constant

import pychastic

import jax.numpy as jnp

problem = pychastic.sde_problem.SDEProblem(lambda x: jnp.array(1.0),lambda x: jnp.array(1.0),0.0,2.0)

solver = pychastic.sde_solver.SDESolver()

trajectory = solver.solve(problem)

trajectory

{'time_values': array([0.,0.01,...]), 'solution_values' : array([0.,0.0082,...]),'wiener_values' : array([0.,0.0082,...])} #some values random

import matplotlib.pyplot as plt

plt.plot(trajectory['time_values'],trajectory['solution_values'])

plt.show()

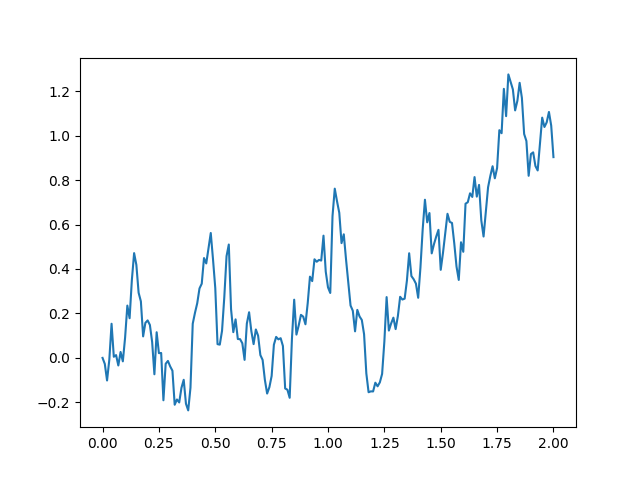

Geometric Brownian motion¶

In this classic example both drift and noise are proportional to current value. Such process is used as model for stock market behaviour.

import pychastic

problem = pychastic.sde_problem.SDEProblem(lambda x: 0.2*x,lambda x: 0.5*x,1.0,2.0)

solver = pychastic.sde_solver.SDESolver()

trajectory = solver.solve(problem)

import matplotlib.pyplot as plt

plt.plot(trajectory['time_values'],trajectory['solution_values'])

plt.show()